Onboarding and channels

Onboarding is where compliance and conversion meet at the same moment. Every identity check that protects you from fraud also adds friction that can lose a customer mid-signup. Know Your Customer (KYC) flows and identity checks sit on this line, and the quality of that flow shows up directly in how many people finish and how many drop off.

Regional assumptions about devices and connectivity change the design completely. In much of sub-Saharan Africa, basic feature phones still dominate, and Unstructured Supplementary Service Data (USSD) carried 63.5 percent of total transaction volume in 2024 because it runs on 2G without an app. A European onboarding flow built for a high-end smartphone and fast broadband simply will not work there. Onboarding quality connects straight to whether the business scales or stalls.

Who owns compliance

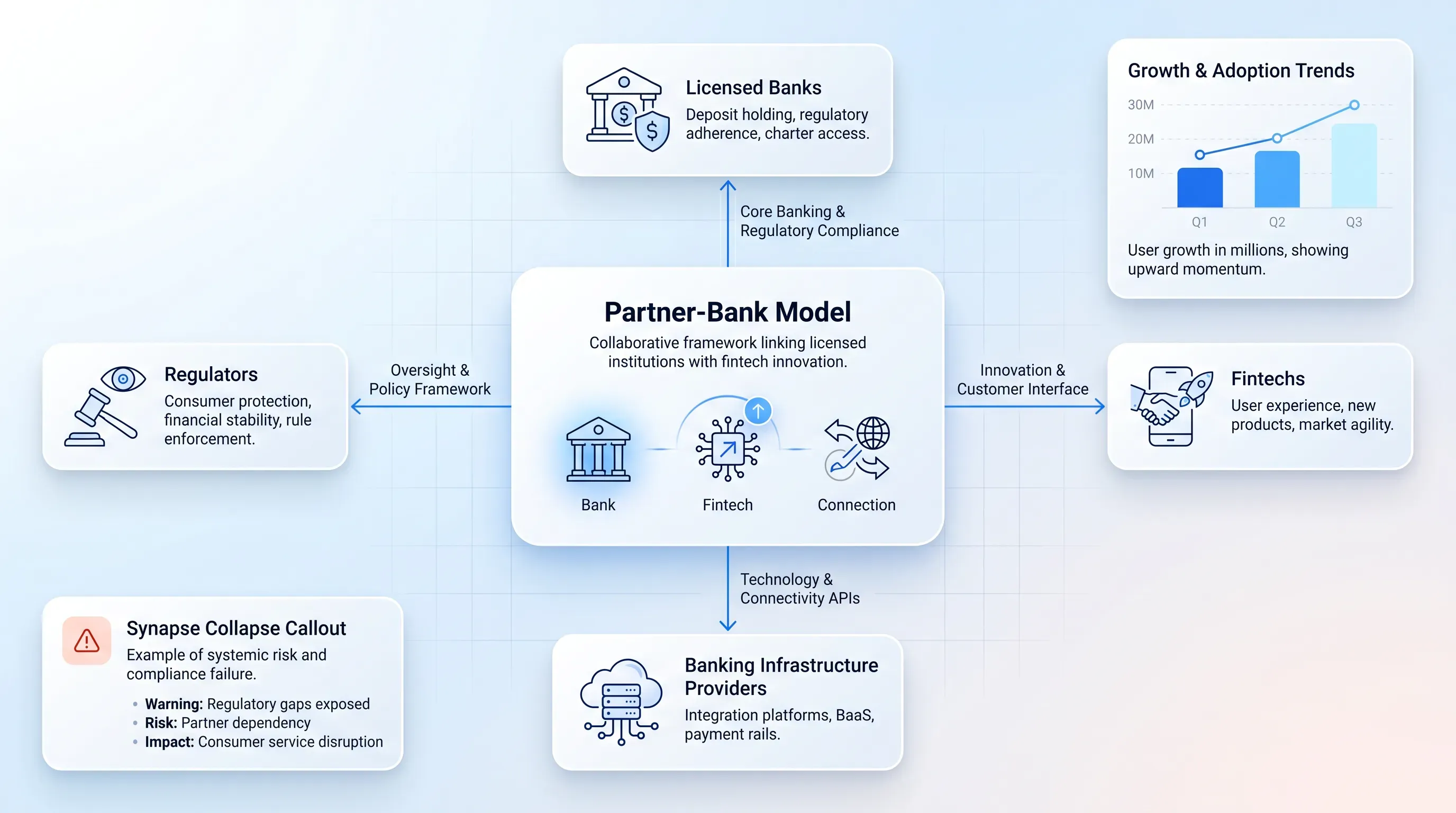

The question of who owns compliance is where founders deceive themselves. The partner bank model creates shared obligations, and in practice the fintech still has to run KYC and monitor transactions for money laundering, even when the licence sits with someone else. The partner carries the regulated activity, but the fintech carries the operational reality of staying compliant.

The Synapse aftermath proved how shared this responsibility is. In June 2024, the partner bank Evolve entered a cease-and-desist order with the Federal Reserve over anti-money-laundering and risk-management failures in its fintech partnerships. The regulator went after the bank, but the fintech banks built on it lost their products and their customers' trust. When compliance fails anywhere in the chain, everyone in the chain pays.

Europe and Africa apply this pressure differently. In the EU, the framework is harmonised and heavy. An electronic money licence runs under EMD2 and PSD2, with PSD3 already agreed and implementation targeted around 2026 to 2027, which means re-authorisation is coming for everyone holding a licence. African markets vary by country, with central banks like Kenya's running sandbox approaches that let innovation move while risk stays managed. The thread running through both is the same. A rented licence creates shared compliance responsibility, and shared responsibility is still yours.

Lending wallets and product reach

The infrastructure you assemble decides which products you can actually offer. Payments are the entry point. Stored-value wallets and lending sit further up the ladder, and each rung changes the risk and compliance picture beneath you. A fintech bank that wants to move from moving money to holding it, or from holding it to lending it, changes what kind of institution it is.

Adding stored value means you now hold customer funds, which pulls in safeguarding rules and the obligation to redeem at par. Adding credit is a larger jump still, because lending introduces balance-sheet risk and capital requirements under a different layer of regulatory scrutiny.

Consider how the ambition maps to the stack:

-

Payments and transfers need rails and a basic ledger, with the lightest compliance load of the three.

-

Stored-value wallets need safeguarding and fund-protection controls, which raises the bar on both infrastructure and oversight.

-

Lending needs a licence or a partner willing to underwrite, plus capital and credit-risk systems the other two never touch.

Product ambition has to be matched to the underlying stack and the licence behind it. A fintech bank that promises credit on infrastructure built only for payments will hit a wall, because the operating model cannot carry the product. Decide what you want to offer first, then build the stack that can actually support it.

Scaling risk for fintech banks

Growth exposes the decisions made at the start. As fintech banks expand across European and African markets, the risks shift from "can we launch" to "can we survive what we built." The early choices about partners and licences, including the rails behind them, either open the door to scale or quietly close it, and by the time the constraint shows up, it is expensive to fix. The risks that matter most fall into a few clear categories.

Dependency on banking infrastructure providers and partners is the first. A fintech bank built on a single sponsor inherits that sponsor's fate, as the firms tied to Synapse discovered when the platform failed. Regulatory shifts are the second, and Europe's move toward PSD3 means licence holders face re-authorisation whether they planned for it or not. Payment concentration is the third risk. A business routing everything through one rail or one processor has a single point of failure that grows more dangerous as volume climbs. Operational strain is the fourth, because systems that handled 10,000 customers do not automatically handle 10 million.

The through-line is that scaling is constrained by the operating model long before it is constrained by the market. Fintech banks that chose a rigid core or leaned on one partner will feel those choices most acutely when they try to expand into a second country with different rails and different rules. The work of scaling is partly the work of unwinding early shortcuts, and the fintech banks that scale cleanly are the ones that left themselves room to change.

Making the right model choice

The correct model is the one that fits your purpose in the market and your appetite for risk. A founder chasing speed in a single country will reasonably lean on the partner bank model and accept the dependency. An institution building for the long term across multiple markets has a stronger case for owning more of the stack, even at the cost of years and capital. The decision is a trade, and naming the trade honestly is most of the work.

The markets themselves keep moving. Europe is consolidating around instant payments and tightening its rules under PSD3, while African markets are building some of the most advanced real-time and mobile-money rails in the world. Both directions reward fintech banks that understand their own infrastructure behind the app. Before you build or pick a partner, define your operating model clearly, because that definition shapes every compliance and infrastructure choice that follows for fintech banks of every size.

Doocat builds the banking software that sits underneath this kind of decision, with a remote banking system covering retail, corporate, e-wallet, and instant-transfer services deployed across markets in Europe and Africa. If you are weighing the core and compliance setup for fintech banks, book a consultation with the Doocat team to pressure-test your operating model before you commit to building or partnering.