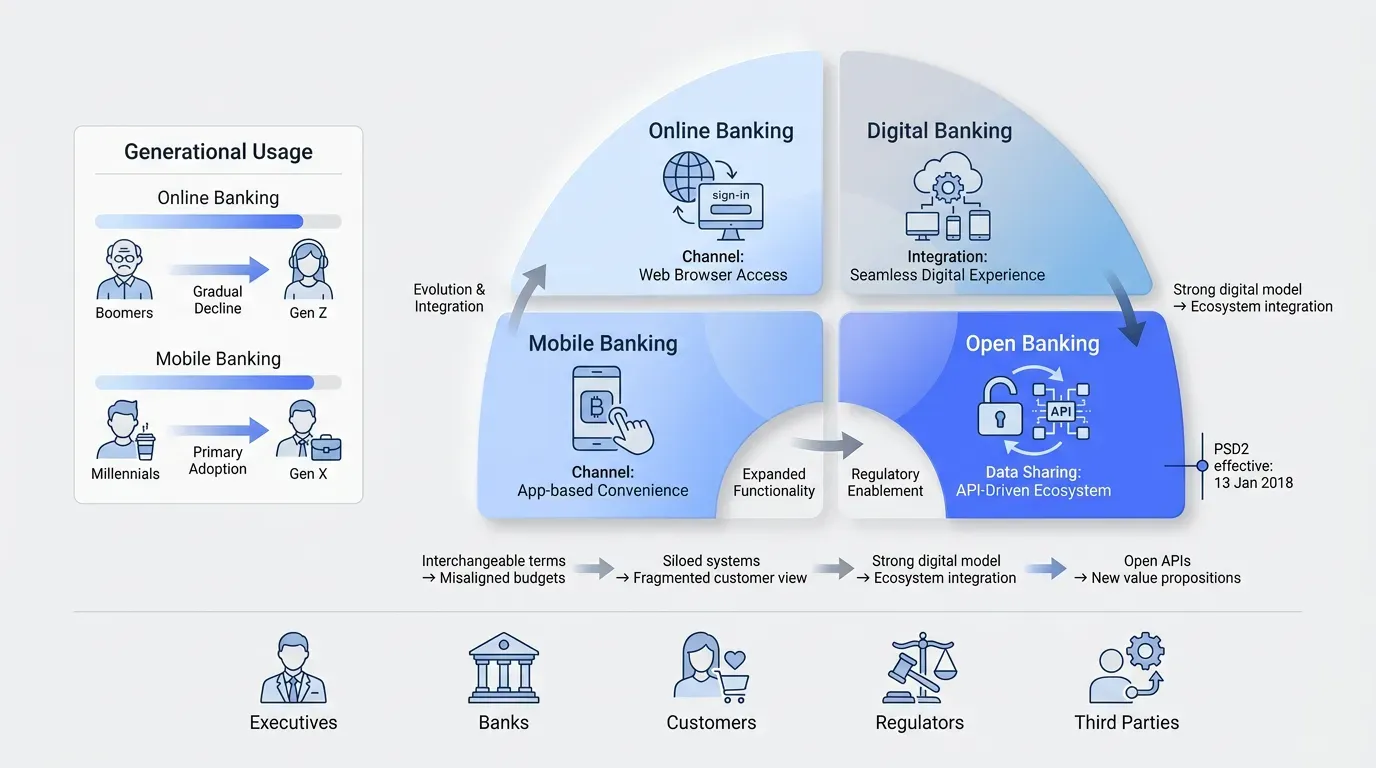

Online, mobile, digital, and open banking

Executives use these four terms interchangeably, and it costs them. Each one implies a different budget and a different owner, with its own regulatory conversation. Treating them as synonyms is how an institution ends up funding a mobile redesign when the actual problem is core integration, or commissioning an open banking program before the underlying digital banking model is in place.

Here is the practical separation:

-

Online banking is a channel: browser-based access to existing accounts.

-

Mobile banking is a channel: smartphone-based access through a native app.

-

Digital banking means the institution-wide operating model that sits above and governs the channels.

-

Open banking is a regulatory and data-sharing layer that extends the perimeter of a digital bank outward to third parties.

An institution can be strong in one and weak in the others. A bank with a polished mobile app and a paper-driven back office is mobile-strong and digital-weak. A bank with PSD2-compliant APIs but a fragmented customer experience is open-banking-compliant and digital-immature.

Online banking

Online banking is browser-based access to existing accounts and transactions. It was the first digital channel most banks deployed in the late 1990s, and for many institutions it remains the workhorse for older customers. The American Bankers Association's 2024 consumer survey found that 41% of Baby Boomers still use online banking via laptop or PC as their primary banking method.

The limits of online banking are scope and experience. It exposes a fixed set of account servicing functions through a web page. It rarely originates products and rarely handles complex servicing; context almost never carries to other channels.

Mobile banking

Mobile banking is smartphone-based access through a native app, with features shaped by what the device can do, like biometric login and camera-based check deposits. Adoption is now broad rather than generational. The same ABA survey found that 64% of Gen Z and 68% of Millennials use mobile banking apps most often, and even 38% of Baby Boomers now prefer mobile apps over online banking on a PC, according to Unblu.

A strong mobile app is necessary and not sufficient. It's the front door of a building. If the building behind it is laid out badly, the front door doesn't save you. Plenty of institutions have shipped beautiful apps that crash into manual back-end work the moment a customer tries to do anything beyond checking a balance.

Digital banking

Digital banking means the connected operating model across onboarding, channels, payments, core, and servicing. It is the thing that decides how the mobile app, the online portal, the branch teller's screen, the contact center's CRM, and the core ledger behave as one system. It sits above any single channel.

When executives say "we need a digital strategy," what they need is an operating model decision at this level. Choosing a new app vendor without that decision is choosing a paint color before you've decided on the building.

Open banking

Open banking is the regulated or voluntary sharing of customer data and payment initiation with third parties through Application Programming Interfaces (APIs). In Europe, it sits on top of the Second Payment Services Directive (PSD2), which came into force on 13 January 2018 and obliged banks to grant licensed third parties access to payment accounts with customer consent. Australia uses the Consumer Data Right. The U.S. has taken a more decentralised path.

Open banking expands the perimeter of a digital bank rather than replacing it. If your digital finance model is solid, open banking lets you plug into a wider ecosystem. If it isn't, open banking just exposes the gaps faster.

How digital banking works across the customer journey

Digital banking is judged at the journey level. Here is what each stage of the lifecycle looks like in practice, and where most institutions still drop the ball.

Acquisition is where prospective customers find the institution and form an intent to apply. In a connected digital finance model, marketing attribution and product eligibility are already wired together when the application starts, and pre-fill data is ready at the same point. Most banks still treat the marketing site and the application form as two disconnected projects.

Onboarding is the single most leak-prone stage. Signicat's Battle to Onboard research found that 68% of consumers abandoned a digital banking application mid-process in 2022, up from 40% in 2016. The reasons are familiar: too much information requested and too much time required, with identity verification that punts the customer to a branch. In a real digital banking model, digital banking means Know Your Customer (KYC) and core account creation happen in one flow, with identity verification handled inside it. In a fake one, the customer is asked to mail in a copy of their passport.

Customer activation and lifecycle management

Activation is the first week or two after the account opens. Did the customer fund it? Did they make a first transaction? End-to-end banking journeys treat activation as a designed flow. They prompt, nudge, and remove the next obstacle before the customer notices it.

Daily use is the boring middle of the relationship, and it's where mobile dominance now shows up. The ABA reported that 54% of Americans now cite online and mobile banking apps as their primary banking method. The question for the institution is whether the app is the same brain as the rest of the bank.

Servicing and lifecycle events are where things break. A customer disputes a transaction or asks about a card replacement, and the journey hits a back-end system that was never wired into the front end. The 64% of consumers who rely on branches for conflict resolution do so because the digital path runs out.