Agent banking operations

Agent networks extend the institution into communities where a branch would never pay for itself. The shopkeeper and the kiosk operator become the cash-in and cash-out points for a microfinance bank that no longer has to build physical infrastructure for every catchment. Done well, agent banking operations also become the primary acquisition channel.

The technology behind agent banking operations is more demanding than it looks. Agent onboarding, device provisioning, real-time transaction visibility, commission engines, and liquidity monitoring all need to run continuously, because an agent who runs out of float at midday loses customers for the institution along with transactions. Letshego's LetsGoBlueBox model in Mozambique, launched in 2016, is one documented example of an MFI building agent banking operations on smartphones with biometric capture, designed specifically for rural low-income segments.

Fraud risk and service quality monitoring complete the picture. Agent banking operations sit closer to cash than any other channel, which makes them the natural target for collusion and identity abuse. Modern platforms flag device anomalies and agent-customer collusion in near real time, which is the only way to scale agent banking operations beyond a few hundred outlets without losing control. The payoff is reach. The IFC Partnership program brought formal financial services to populations across Sub-Saharan Africa by treating banking agents as the front line of customer acquisition.

Payments and integrations

Payments are where the microfinance bank meets the rest of the financial system. The payments layer connects to mobile money providers, card schemes, national switches, and instant payment rails, and it decides whether moving money in and out of a customer's wallet feels instant or feels like a complaint waiting to happen.

The rails are also widening. AfricaNenda's State of Inclusive Instant Payment Systems report counts four IPS that already include banks, MMOs, MFIs, and non-bank PSPs as direct participants, with GIMACPAY in the CEMAC region uniting 105 participants, of which 14 are microfinance institutions. The Mojaloop Foundation pushes the same logic further with open APIs so that a customer of the smallest MFI can transact instantly with a customer of the largest bank.

Good payment architecture is open by default. APIs and clear settlement and reconciliation workflows are what let the institution plug into new rails as they appear without rebuilding the stack each time. Poorly designed payment flows show up as failed transactions and suspended balances, which directly erodes stickiness. The opposite is also true. When payments work, customers route more of their financial life through the institution because it's where their money actually moves.

Reporting, analytics, and compliance

The top layer turns everything below it into something a regulator or a credit committee can act on. Central bank reporting, Anti-Money Laundering (AML) monitoring, audit trails, portfolio analytics, and board dashboards all live here, and they all depend on the data being clean at the source.

A unified data layer is what makes this section work. When the core, loan system, channels, and payments all feed a single warehouse, the credit team and the finance team stop arguing about whose numbers are right. WSBI's case study work on African banks makes the point bluntly: institutions that built a dedicated analytics function and let customer data lead product decisions outperformed those that didn't.

Compliance is the operating baseline. Regulators expect on-time, accurate filings, and they increasingly expect AML monitoring that runs continuously rather than as a monthly batch job. Above that floor, analytics is where growth lives. Cohort behaviour, channel mix, segment profitability, and early-warning credit signals are all readable from the same data, and the institutions that read them well find growth opportunities the rest miss.

Running a branch-light operation

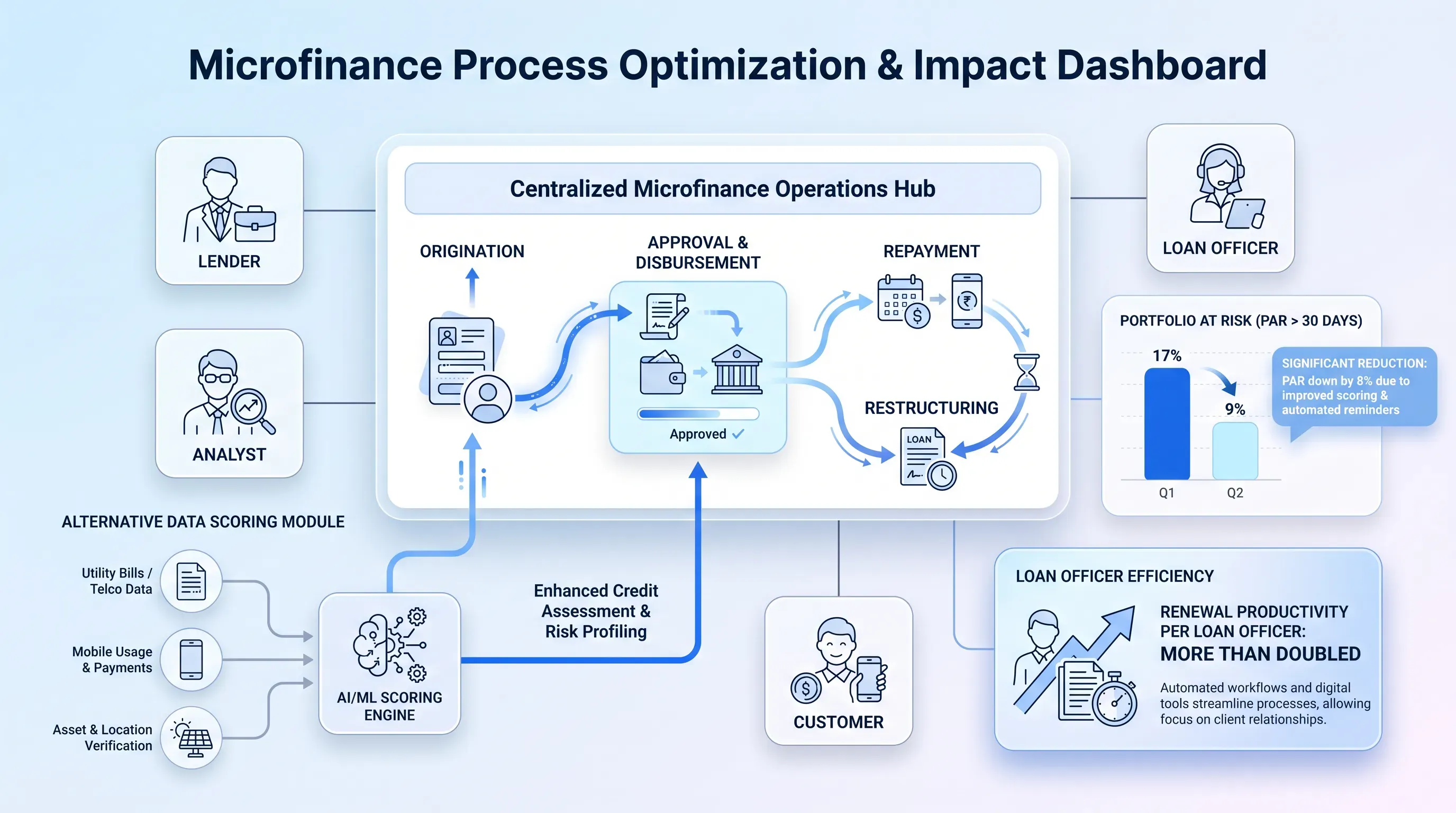

Bring the layers together and a branch-light microfinance bank starts to look concrete. A customer in a rural area meets an agent who captures her biometrics and ID on a tablet. The onboarding layer pushes her record into the core. She applies for a small working capital loan through Unstructured Supplementary Service Data (USSD) on her feature phone, and the loan system runs an alternative-data score in seconds. Funds land in her mobile money wallet the same morning. She repays weekly through the same wallet or by handing cash to the agent who onboarded her.

The process avoids a branch visit and a paper file while keeping the loan officer from driving 40 kilometres for a signature. Redian Software's deployment with ABC Finance in Cameroon documents what this can do in practice: an 85% reduction in loan processing time, from 14 days to 2, alongside a 60% drop in operational cost per transaction within 12 months of moving to a digital core with integrated mobile money.

The technology is only half the change. Branch staff become remote support and agent supervisors. Credit committees move from paper packs to dashboards. Risk teams shift from spot checks to continuous monitoring. Organisations that try to bolt branch-light operations onto an unchanged operating model find the savings disappear into shadow processes, which is why the process work matters as much as the platform work.

Evaluating your current stack

The practical question for any executive reading this is simple. Does your current setup actually support the growth and reach you're aiming at, or is it quietly capping both?

Map your current systems against the layers in this article and mark where each one sits. The gaps that matter most are the ones blocking remote service delivery, because those are the ones capping reach. A microfinance bank with a core banking for MFIs platform that cannot expose APIs will hold itself back from the customer numbers the board is asking for. The same constraint appears when the loan system cannot ingest alternative data or agent banking operations lack real-time visibility.

Doocat builds banking software for microfinance bank operations, with core banking for MFIs, lending, mobile, and agent banking operations in a single integrated platform. If you're auditing your stack against the layers in this article and want a second view from a team that has done this work with other microfinance bank clients, reach out to Doocat to start that conversation.