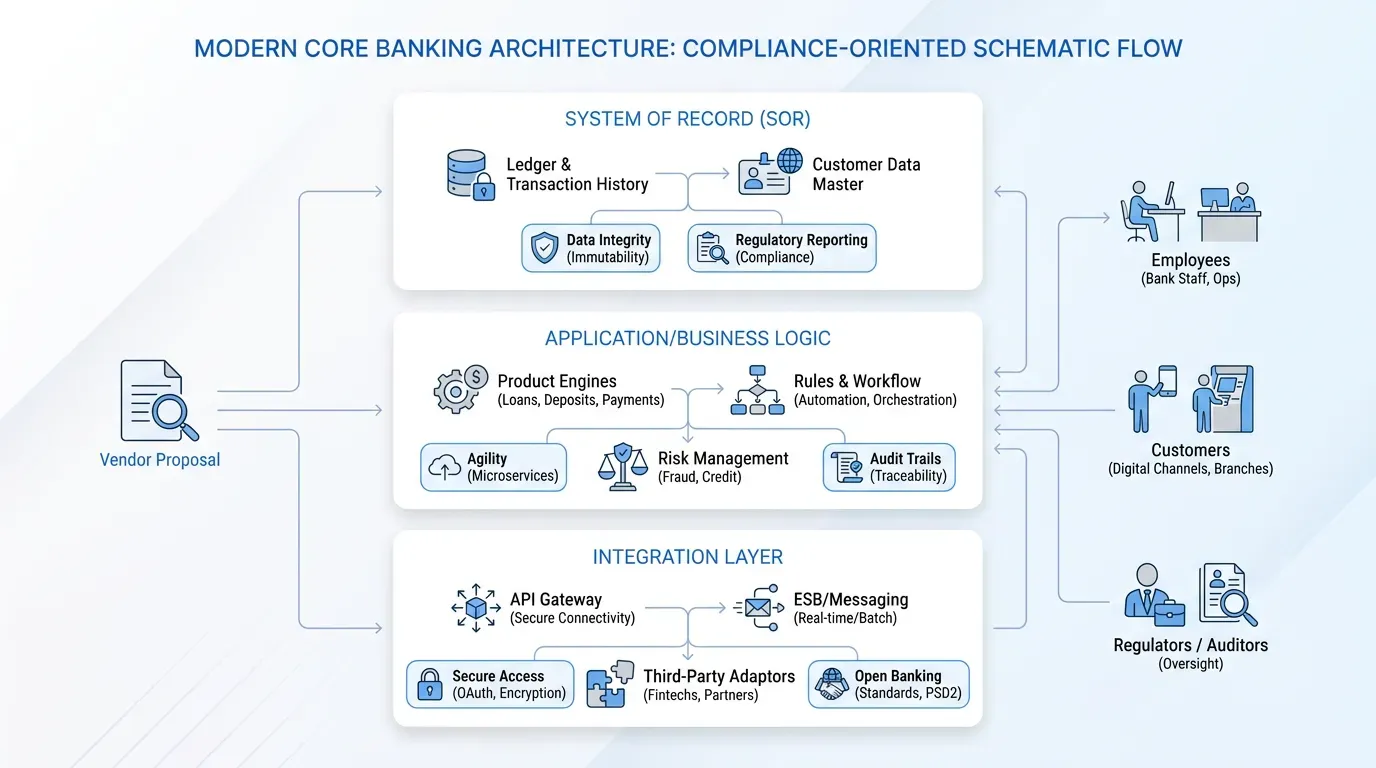

Database and core ledger layer

This is the system of record where account balances and transactions live. It runs on a relational database like Oracle Database or PostgreSQL, or on cloud-managed equivalents. The database layer is rarely negotiable in functionality, but the commercial terms around it are wildly misunderstood.

Confirm in writing who pays for the database license and who hosts the environment, with backup and restore testing responsibility named in the same document. A vendor proposal that quotes "core banking software" without specifying Oracle license costs is hiding a six- or seven-figure line item. This is the foundation of the core banking architecture, so treat the cost breakdown with the same rigor you'd treat a loan covenant.

Application and business logic layer

This is where products, interest rules, fee structures, and approval workflows live. It's also where contracts go vague. Who configures a new microloan product? Who tests it? Who signs it off as compliant with the local regulator's interest cap?

In the implementation responsibility matrix, every product variant should have a named owner for build and test, with approval responsibility stated separately. If the vendor's proposal says "standard products included," ask which exact products and parameter sets are covered, and ask what counts as a customization. A group lending product with weekly repayments and a co-borrower guarantee is not the same as a vanilla term loan, even though both are "loans" on the brochure.

Channel and integration layer

This layer is where APIs and middleware live, along with connections to mobile banking, agent networks, ATMs, payment switches, and regulatory reporting. It's also where most scope disputes happen. The On-Point analysis of core banking projects recommends scheduling 50 to 100 percent of the implementation effort just for integration work. Most buyers budget a fraction of that.

Before signing, list every external system your institution touches. Payment switches, SWIFT, national instant payment rails, credit bureaus, tax authorities, KYC providers, SMS gateways, and your existing CRM. For each one, specify who builds the connector and who owns the test cases, with payment responsibility set for any third-party API change. This is the layer where the core banking architecture meets the meaning of core banking solution in reality, and reality is expensive.

Modules included and excluded

Vendors package modules differently, and the included list almost never matches your operating reality. "General ledger included" can mean a basic chart of accounts without the multi-entity consolidation your group structure needs. "Loans module" can mean term loans while excluding specialized cases such as group lending with joint liability and Islamic financing with profit-sharing; the rescheduling workflow your collections team actually uses can also be outside scope.

Read the module list like a contract lawyer reads warranties. Ask the vendor to list, in writing, every product type and report that's covered as standard, with workflow coverage stated separately. Then ask what happens to the items that aren't. The American Bankers Association's 2024 Core Platform Survey found that 35% of US banks are dissatisfied with their current core process, and a large share of that dissatisfaction traces back to modules that sounded right in the demo and disappointed in production.

Don't assume general categories cover institution-specific variations in the meaning of core banking solution. They rarely do.

Integration ownership and the implementation responsibility matrix

Integrations are the single biggest source of post-contract disputes. The vendor assumed the buyer would deliver the payment switch API spec. The buyer assumed the vendor would handle it. Neither did. Six weeks before go-live, the project manager discovers the gap, and the change request lands.

This is what an implementation responsibility matrix prevents. It's a structured table based on the RACI framework that lists every task in the project and assigns one of four roles to each party: Responsible, Accountable, Consulted, Informed. Jamilyn Trainor, senior project manager at Müller Expo Services International, told Project-Management.com that RACI matrices "force owners of the project to clear timelines for approvals, provide clarity, push decisions faster, and call out gaps before they become failures."

For a core banking project, the implementation responsibility matrix should cover every integration point, every test cycle, every regulatory submission, and every handover from build to operations. And it must include third parties. If your national payment switch operator needs to certify the connection, put their name on the matrix. If the credit bureau requires a 90-day testing window, that goes on the matrix too.

A few rules for using the implementation responsibility matrix well:

-

One Accountable role per task, never two. Shared accountability is no accountability.

-

Update the matrix whenever scope changes.

-

Get the third parties to sign their rows along with the vendor and the buyer.

Vendors who push back on signing an implementation responsibility matrix are telling you something. Listen.