Why cash operations break at scale

You run a bank or microfinance institution (MFI) where cash management systems were never the problem when everything sat under one roof. One branch and one safe, with a person who knew the count by heart. Then you grew to dozens of branches and a field of agents, and the methods that held together at one location started splitting at the seams. The count still happens, but you can't see it until it's too late to act on.

The failure modes are specific, and you recognize them. You don't know the live cash position at half your locations until end-of-day reports land. Reconciliation happens in spreadsheets after the fact, where matching branch cash against agent cash against wallet settlements eats days of staff time every month. A manual spreadsheet process can run 40 to 80 hours a month and add several days to close, with matching rates that land closer to 78 to 85% when done by hand. And exceptions such as variances and failed settlements bounce between branch staff and head office with no clear owner.

These are symptoms of one root cause. You're treating cash as an accounting record to reconcile after the money has already moved, so live operational control disappears while it's moving. The Women's World Banking cash management toolkit defines the discipline as the planning and control of cash through procurement, whether it sits in a branch safe or in the hands of field staff. Control is the word that breaks at scale. The rest of this guide treats that as the problem to solve.

What cash management systems actually do

If you know your operations cold but you're new to cash management systems, start with the boundary. Your core banking system is the system of record. It processes transactions and updates balances while it maintains the general ledger, and it answers the question of what each account holds after the money has settled. It records the truth, which is exactly what an accounting record is supposed to do.

A cash management system sits on top of that and answers a different question: what is happening to physical and electronic cash across your network right now, and who needs to act. It's an operational control layer. The work it handles is live-position visibility and reconciliation workflows, with approvals on cash movements and exception handling when something doesn't match. The ledger tells you the balance. The control layer tells you that a branch is about to run short or that an agent's float is stranded; it also catches yesterday's wallet settlement when it breaks against the branch deposit.

This distinction matters when you start talking to vendors. Some products are reporting tools bolted onto core banking, dashboards that summarize what the ledger already knows. Others are built to run the operation as it happens. The difference shows up the moment cash crosses a branch boundary or moves between an agent and the institution, because that's where the ledger goes quiet and the control layer has to take over. Knowing which one a vendor is selling you is the first thing to settle.

Core capabilities to evaluate

The cleanest way to compare competing cash management systems is to stop reading feature lists and score every shortlisted product against the same operational capabilities. Features describe what a system has. Capabilities describe what it does when your network is under load on a busy Friday afternoon. The four below are the minimum bar for a system that holds up across branches and agent networks, including wallets. Ask the same questions of every vendor and write down the answers, because the gaps surface fast when the responses sit side by side.

Branch cash visibility

Real-time branch cash visibility is the foundation. Everything else in cash management systems depends on knowing, at any moment, how much cash sits where. What you should demand is a live position per location and agent float tracked the same way, with configurable thresholds that fire an alert before a branch runs short or sits on idle excess. Idle cash is not free. In one documented case, transfers between a central account and a rural bank account took up to seven days each direction, and someone has to carry the cost of interest on money sitting in transit.

Here's where vendors separate. A system that offers end-of-day reporting tells you this morning what happened yesterday. A system with real-time branch cash visibility tells you now, while you can still reroute cash or hold a disbursement.

When a vendor demos a dashboard, ask the questions that expose the difference:

-

How often does a position refresh, and is it event-driven or a scheduled batch?

-

What happens to branch cash visibility when a branch goes offline, and how does the position reconcile when connectivity returns?

If the honest answer is that everything updates at end of day, you're looking at a reporting tool. The distinction between real branch cash visibility and after-the-fact reporting is the single fastest way to thin a shortlist.

Reconciliation workflows

Strong reconciliation workflows are where a distributed system earns its cost. What good looks like is automated matching across branch cash and agent cash, with wallet settlements included and breaks surfaced clearly instead of buried. Automation moves the numbers. One finance team cut reconciliation from about 20 hours a month to 3 after connecting fragmented data and automating the matching, while cutting errors by 90%. A well-tuned automated setup reaches a matching rate of 95% or higher once your main flows are modeled.

But a vendor demo runs on clean data, and your network does not. So test reconciliation workflows against your messiest real scenario: the agent who banked late and the wallet settlement that arrived split across two days, with the wrong-reference branch transfer in the same file. The number that matters is how much manual effort the system actually removes from your worst week. Judge two things while you watch. First, how cleanly the reconciliation workflows route a break to the person who can resolve it. Second, where human review still belongs, because some judgment calls should never be automated away.

Exception queues

Reconciliation breaks and failed settlements become exceptions. Every cash variance becomes an exception too, and exception handling is where distributed cash operations quietly leak time and trust. The system has to surface each exception and track it to resolution under a named owner. What you don't want is a generic alert dump, a feed of notifications nobody owns and everybody scrolls past.

Look for three things in the cash management systems exception layer. Clear ownership, so every item has a named person attached. An escalation path, so an unresolved variance climbs to a supervisor on a timer rather than aging silently. And a complete audit trail, because separating the people who originate transactions from the people who reconcile them to the ledger is a basic control the FDIC names directly. When a cash variance sits unresolved for a week, trust between a branch and head office erodes, and that erosion is harder to reverse than the variance itself.

Approvals and controls

The control layer is what protects a distributed network from the inside. You need configurable limits on cash movements and maker-checker flows for adjustments across every location, with segregation of duties built into both. Maker-checker separates the person who initiates a transaction from the person who approves it, so no single individual controls both the creation and the validation of a cash movement. The possibility of fraud drops the moment two people are required to complete a transaction.

The trick is applying these controls without grinding daily operations to a halt. A control that forces head-office sign-off on every routine float top-up will be worked around within a week, and a worked-around control is no control at all. So judge flexibility against your real structure. Can limits differ between a metro branch holding large balances and a rural agent operating on a few hundred dollars of float? Can a low-value, routine movement clear on a single approval while a large adjustment demands two? If the system forces one rigid rule across every location, it will either choke your busy branches or leave your exposed ones under-controlled.

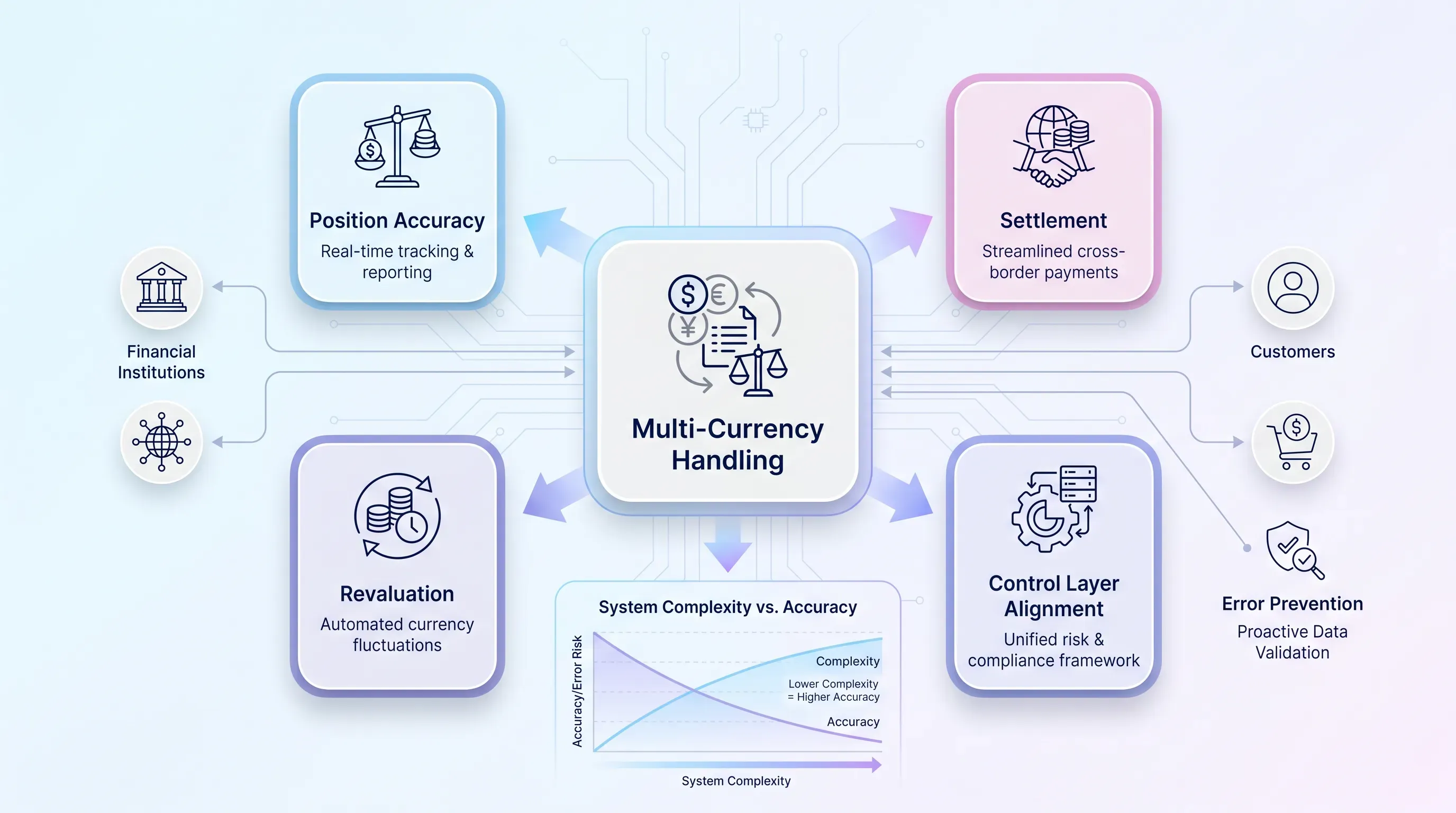

Handling multiple currencies

If your network spans currencies or sits along a border region, multi-currency handling moves from nice-to-have to essential. The system has to hold an accurate position per currency and settle across currency lines, with revaluation handled as rates move and the spreadsheet bridge removed. Core banking ledgers like Oracle FLEXCUBE already support reconciliation and account revaluation at the GL level, so your control layer has to align with that rather than fight it.

Be honest about your own footprint before you weight this heavily. A single-currency MFI operating in one country can treat multi-currency as optional and avoid paying for complexity it will never use. An institution serving a border economy, where customers transact in two currencies across the same counter, has to treat accurate per-currency positions as a hard requirement. The failure mode to watch for is a system that technically supports multiple currencies but forces manual workarounds at the settlement step, which is exactly where the errors you're trying to eliminate creep back in.

Integrating with core banking and wallets

Now the second worry: integration. A cash management system's reliability depends on its connection to the systems around it, and integration quality decides whether the thing delivers day after day. Ask your IT team and your vendor the right questions, because this is where deployments quietly fail.

In practical terms, the system connects to core banking and to wallet settlement rails through Application Programming Interfaces (APIs), and data flows in both directions. In cash management systems, position and transaction data flow in so the control layer can see what's happening. Approved movements and adjustments flow back out to post against the ledger. The questions to put to your vendor are concrete. How often does data sync, and is it real-time or batched? What authentication does the connection use, given that invalid keys and expired tokens are among the most common integration failures? And critically, what happens when a sync fails midway?

That last question matters most, because the failures are predictable. Payments integration breaks on point-to-point sprawl and connections built from scratch instead of reusable adapters, and the break surfaces when a live transaction is expected to go through. Wallet settlement adds its own pressure. Globally, mobile money now moves over $4.6 billion daily, and any system touching those wallet settlement rails has to handle a failed settlement without silently dropping it. Ask the vendor to walk through one failure scenario end to end. If they can't, your IT team will be debugging it in production.

Rolling out without disruption

A big-bang switch across a live network is the fastest way to lose the trust you need from branch staff. Cash moves through every location, so the rollout has to be controlled and reversible, with stages you can pause. Gartner attributes 80% of unplanned downtime to poorly planned IT changes, which is the entire argument against flipping a switch and hoping.

The sequence that works moves in steps you can pause:

-

Pilot in a few branches that represent your real range, with at least one branch that has shaky connectivity, so problems surface where you can contain them.

-

Run the new system in parallel with your existing process, so reconciliation ties out cleanly against the ledger before anyone depends on it alone.

-

Expand wave by wave only after each group hits its targets, with rollback plans ready at every stage.

The BCG team that documented a successful bank automation rollout described accelerating into multiple waves in parallel only after the early waves proved out, backed by a central group that owned training and change management. That last part decides whether the system sticks. Branch and agent staff have to trust the cash management systems interface more than the spreadsheet they've used for years, and that trust comes from training that creates early wins they can see and from a clear answer when something looks wrong. As BCG noted, staff anxiety during a change of this size can't be eliminated but can be managed through direct, regular communication.

Choosing the right cash management systems

The decision comes down to three weights. Score each shortlisted product against the capabilities covered earlier and the reality of rollout across your network, with integration quality against your core banking and wallet rails treated as part of that score. Let the operational-system lens decide ties. A product that runs your cash as it moves beats one that reports on it after the fact, regardless of which has the longer feature list.

Your immediate next step with cash management systems is concrete: build the scoring sheet and put your real numbers in front of each vendor, with your messiest scenarios included so the answers separate the field.

Doocat builds banking software for MFIs, with agency banking modules for mobile delivery alongside core banking on a microservices architecture that handles cash management across distributed branches and agents. Before you select among competing cash management systems, map your current cash routines, branch by branch and agent by agent, then book a demo and score what you see against the capabilities in this guide.